ZZP vs BV in the Netherlands (2026): Which Business Structure Is Right for You?

If you're starting a business in the Netherlands, one of the first decisions you'll face is whether to operate as a ZZP or set up a BV. The right structure affects your tax position, liability, pension planning and long-term flexibility.”

We get this question constantly. From US entrepreneurs coming in on a DAFT visa, to experienced freelancers who've been ZZP for years and are wondering whether it's time to make the switch, to expats setting up here for the first time with their employer.

The honest answer is: it depends. But the good news is that the decision comes down to a handful of clear factors, and once you understand them, it's not complicated. Let us walk you through it.

What exactly are we comparing?

In the Netherlands, the two most common structures for self-employed people and small business owners are:

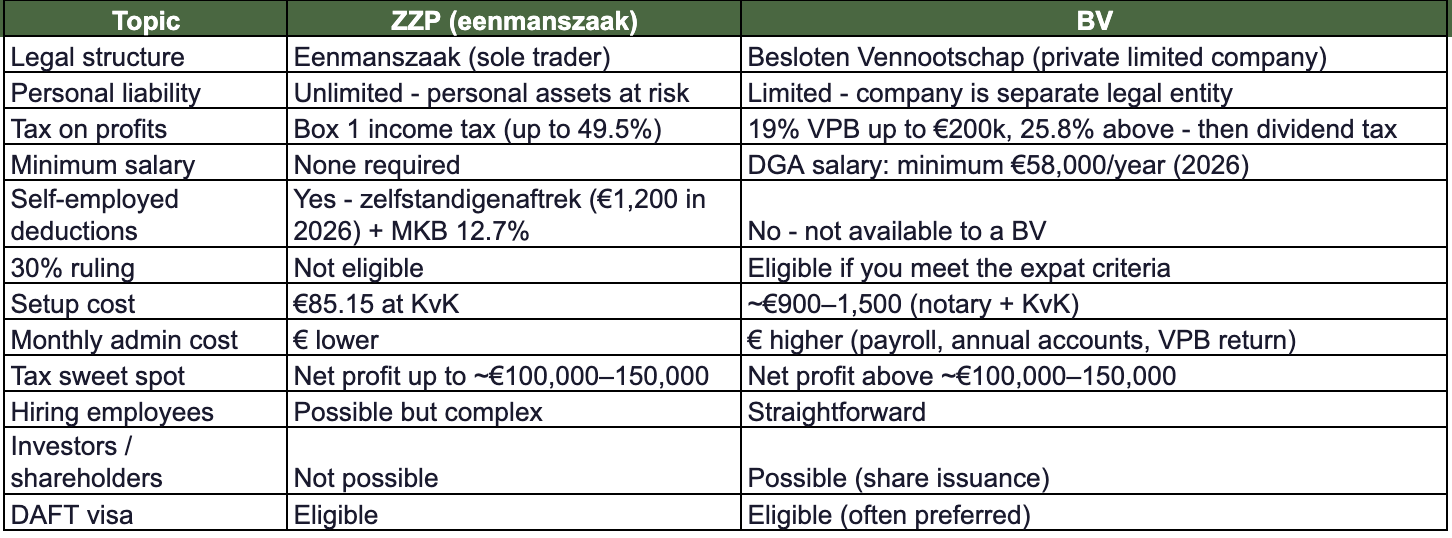

ZZP (zelfstandige zonder personeel) — this is a sole trader registered as an eenmanszaak at the Chamber of Commerce (KvK). There is no legal separation between you and your business. Simple to set up, no minimum capital required, and most freelancers start here.

BV (besloten vennootschap) — this is a private limited company, similar to a UK Ltd or US LLC. The BV is a separate legal entity. You become a director and usually the sole shareholder. It requires more administration, but it offers liability protection and tax advantages at higher profit levels.

t

Side-by-side: the key differences

The tax question - this is usually what it comes down to

One of the frequently asked questions: 'At what profit level does a BV make sense?'

The answer in 2026 is roughly €100,000–150,000 in annual net profit, depending on your situation.

Here's why.

As a ZZP'er, you benefit from:

Zelfstandigenaftrek (self-employed deduction): €1,200 in 2026. Important note: this has been falling steeply - it was €7,280 in 2021. It will decrease further to €900 in 2027. If you've been ZZP a while, you'll have noticed this.

Startersaftrek: an extra €2,123 on top of the zelfstandigenaftrek - available for three years during your first five years in business. Very useful in the early stages.

MKB-winstvrijstelling: 12.7% of your taxable profit is exempt from tax. This applies after the other deductions.

To qualify for the above, you must meet the urencriterium — at least 1,225 hours per year working in your business, have multiple clients, and meet a few other criteria. If you don't meet these, your tax position is much less favourable.

As a BV, the structure works differently:

Your BV pays vennootschapsbelasting (VPB / corporate tax): 19% on profits up to €200,000, and 25.8% on anything above that.

You must pay yourself a DGA salary (directeur-grootaandeelhouder salary). In 2026, this is €58,000, unless you can justify a lower amount based on comparable market salary, limited profitability, or the company’s financial position.

That salary is taxed as Box 1 income - just like employment income.

Any remaining profit after corporate tax can be distributed as a dividend, taxed in Box 2 at 24.5% on the first €68,843 and 31% on anything above that.

The BV can retain earnings inside the company and delay distribution, which gives you flexibility - useful if you plan to reinvest, save for a pension inside the company, or buy property.

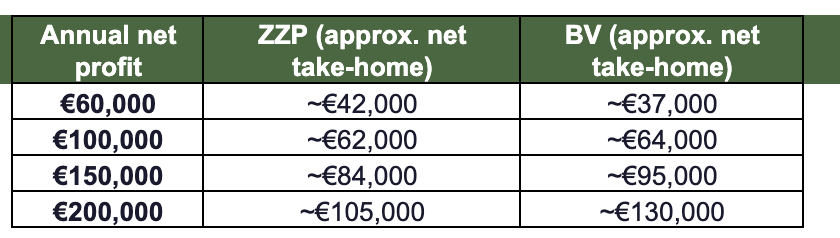

Approximate net take-home comparison (indicative figures for 2026)

Make it stand out

These are illustrative - your actual outcome will vary based on your deductions, 30% ruling eligibility, dividend strategy and more.

But they give a useful sense of direction; below ~€100,000 in profit, the ZZP wins on simplicity and tax. Above that threshold - especially above €150,000 - the BV starts to pull ahead meaningfully, and the more you earn, the bigger the advantage becomes.

The 30% ruling - a game changer if you qualify

If you're an expat who has recently moved to the Netherlands and meets the criteria, the 30% ruling can significantly change the ZZP vs BV calculation.

The 30% ruling lets your employer (in this case, your own BV) pay up to 30% of your gross salary tax-free as a cost reimbursement. This means if you're earning €80,000 gross, €24,000 of that is untaxed. The effective tax rate on your total package drops dramatically.

Crucially, the 30% ruling is only available through a BV. You cannot apply for it as a ZZP/eenmanszaak. So if you're eligible, this alone often tips the decision toward a BV - even at profit levels where a ZZP would otherwise be competitive.

Liability protection - often underestimated

This is a point many people overlook until something goes wrong.

As a ZZP'er, you and your business are legally the same entity. If your business runs into debt, is sued, or has a contract dispute, your personal assets - your savings, your car, potentially your home — are on the line.

As a BV, the company is a separate legal person. Your personal liability is generally limited to what you've invested in the company, unless you've personally guaranteed loans or acted negligently as a director (aansprakelijkheid voor bestuurders).

For most service-based freelancers, the risk is relatively low day-to-day. But the moment you're signing significant contracts, working in regulated industries, or carrying meaningful business liabilities, the protection a BV offers is real and worth paying for.

The DAFT visa - does it affect your choice?

If you're a US citizen living in the Netherlands under the Dutch-American Friendship Treaty (DAFT), your visa ties you to being self-employed. Both a ZZP and a BV can qualify for the DAFT, but there are nuances.

With a ZZP, the setup is simpler. You register your eenmanszaak with KvK, meet the IND's investment threshold (~€4,500), and you're good.

With a BV, you are technically an employee of your own company - but the IND accepts this for DAFT purposes. The BV route is increasingly common among US clients we work with, especially once they grow beyond the startup stage.

Financial statements for IND renewals: whether ZZP or BV, your accountant needs to prepare these. For the BV, this means annual accounts filed at KvK. For a ZZP, a simpler income/equity statement usually suffices.

If you're a DAFT holder thinking about switching from ZZP to BV, coordinate this carefully with your accountant and immigration advisor. Timing matters.

Practical considerations — beyond the tax numbers

Setup and ongoing costs

Setting up a ZZP costs around €85 at KvK and takes a day. A BV requires a notary to draft the deed of incorporation - expect €900–1,500, plus KvK registration. Ongoing, a BV costs more to run: payroll administration, annual accounts, VPB return, and filing at KvK all add up. Budget an extra €2,000–5,000 per year in accounting costs compared to a ZZP.

Invoicing and VAT

Both structures charge BTW (VAT) on their invoices - currently 21% for most services, 9% for certain categories, and 0% for exports.

Pension

Neither structure forces you to save for a pension, but the BV gives you more flexibility: you can leave money inside the company and eventually draw it down, effectively using your BV as a pension vehicle. As a ZZP'er, you're fully responsible for your own pension - put money aside in a lijfrente or bank savings product (banksparen), and claim the tax deduction.

Switching later

You can convert a ZZP to a BV later (called a geruisloze inbreng if done correctly, meaning no immediate tax hit). However, it's more complex and expensive than starting as a BV from day one. If you're already earning well and planning to grow, starting with a BV from the outset often makes more sense.

So - which one should you choose?

Here's how I think about it with clients:

Choose ZZP if:

• You're just starting out and want to test the market

• Your expected annual profit is below €100,000

• You have multiple clients and meet the urencriterium

• You're not eligible for the 30% ruling

• You want to keep admin simple and costs low

• You don't carry significant liability risk

Choose BV if:

• Your annual profit is consistently above €100,000–150,000

• You're eligible for the 30% ruling

• You want to protect your personal assets

• You plan to hire employees

• You want to bring in investors or co-founders

• You want to retain profits inside the company for reinvestment or pension

• You're planning to hold other companies (holding structure)

And if you're somewhere in the middle - earning €80,000–120,000, not sure about the 30% ruling, wondering whether growth is coming - that's exactly when it's worth sitting down for a proper calculation rather than going on a rule of thumb.